By Alexander Arnon

US production of crude oil has more than doubled since 2008.1 Starting in the mid-2000s, the application of horizontal drilling and hydraulic fracturing to tight oil formations led to a surge in US supply known as the shale boom. In this post, I discuss the shale boom’s impact on the relationship between business investment and the price of oil.2 I then estimate the effect of the recent rise in oil prices on investment in 2018. I find that oil prices might even account for most of the increase in the growth rate of investment in 2018.

Business Investment After the Shale Boom

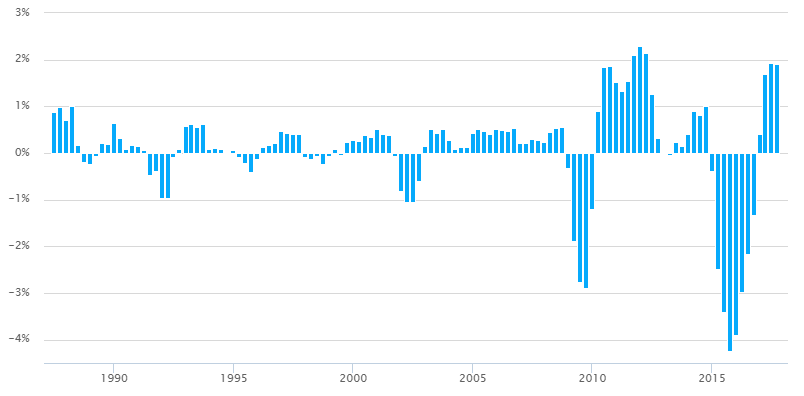

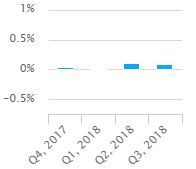

Oil production is capital-intensive. As US production expanded rapidly over the last decade, the oil sector’s importance as a driver of business investment grew in tandem. Figure 1 shows the contribution of oil-related assets to growth in private nonresidential fixed investment. Oil’s direct impact on investment increased sharply around the beginning of the shale boom and has remained significant, though not always positive, since then.

Note: Oil-related assets consist of petroleum and natural gas structures and exploration, mining and oilfield machinery, and railroad equipment.

Sources: PWBM, BEA.

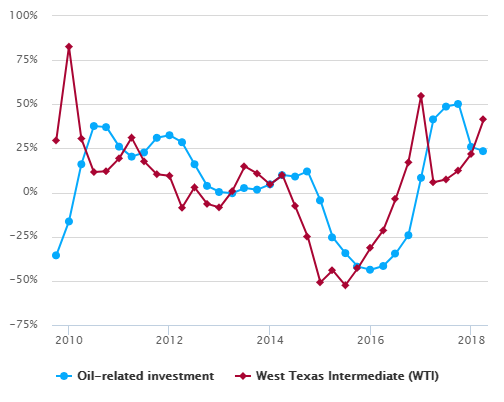

One implication of the oil sector’s increased importance is a change in the relationship between the price of crude oil and US business investment. Figure 2 shows that growth in oil-related investment generally tracks changes in the price of oil with a one- or two- quarter lag. After the price of oil collapsed in 2014, oil-related investment dropped sharply, subtracting nearly three percentage points from growth in total business investment in both 2015 and 2016. When the price rebounded in 2017, so did the oil sector, adding 1.5 percentage points to growth in investment. While oil-related investment is naturally tied to the price of oil, the magnitude of these impacts is much larger than was typical before the shale boom. As a result, changes in the price of oil are now an important driver of changes in overall business investment.

Sources: PWBM, BEA, FRED.

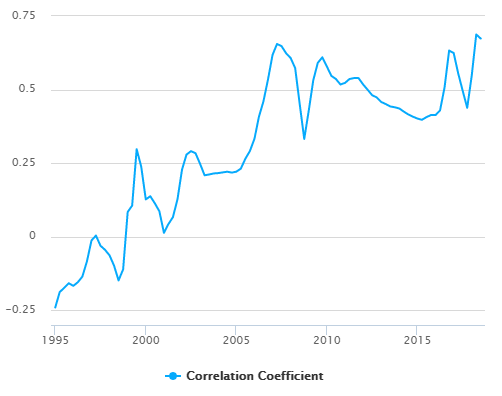

Note: Rolling correlation between year-over-year changes in nonresidential investment and lagged year-over-year changes in the price of WTI.

Sources: PWBM, BEA, FRED.

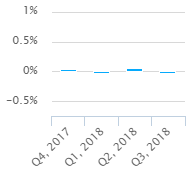

Figure 3 provides further suggestive evidence of the increased sensitivity of investment to oil prices. The figure shows the time-varying correlation between business investment and the price of oil over the last three decades. Prior to the shale boom, there was no consistent relationship: rising oil prices sometimes coincided with increases in investment, and other times with decreases. As the boom unfolded over the course of the 2000s, however, a substantial positive correlation emerged.

The Impact of Rising Oil Prices on Investment in 2018

The price of West Texas Intermediate (WTI), a medium crude oil used as a benchmark for US production, rose from less than $50 per barrel in the third quarter of 2017 to roughly $70 per barrel in the third quarter of 2018.3 Over the same period, growth in business investment picked up. Nonresidential investment grew seven percent year-over-year in the third quarter of 2018, up from five percent over the same period in 2017 and less than one percent in 2016.

To get a sense of how much the 40 percent rise in the price of oil may have contributed to the increase in investment, I estimate a simple statistical model of the determinants of investment and use it to simulate what would have happened if the price of WTI had been stable.

Oil production is the most direct channel through which the price of oil affects investment, but not the only one. Oil is an important input in some industries, and higher prices mean higher costs. Rising prices also crowd out consumer demand for non-energy goods and services, which reduces businesses’ need to invest. To account for these various channels, the model differentiates across ten different types of equipment and structures investment and allows the effect of oil prices to vary for each.

For simplicity, I assume that the only source of investment other than oil-related activities is industrial demand, captured by industrial production in the manufacturing sector.4 Its effect also varies by type of asset. Changes in the price of WTI and in manufacturing production can affect investment contemporaneously or with a lag. I also include year-fixed effects.

Sources: PWBM, BEA.

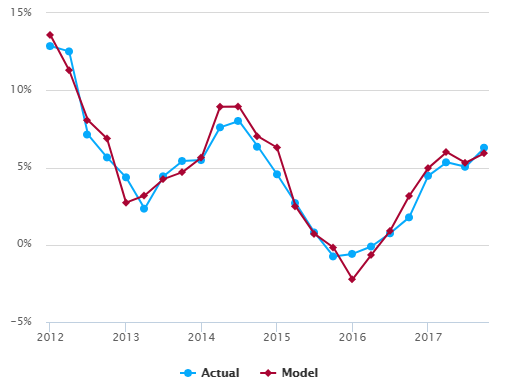

I estimate the model over the period since 2012 using the ten categories of equipment and structures available at quarterly frequency in the National Income and Product Accounts.5 Figure 4 shows how the model matches the data in the estimation sample. Though far from perfect, this simple specification accounts for much of the variation in the growth rate of investment over the last five years.6

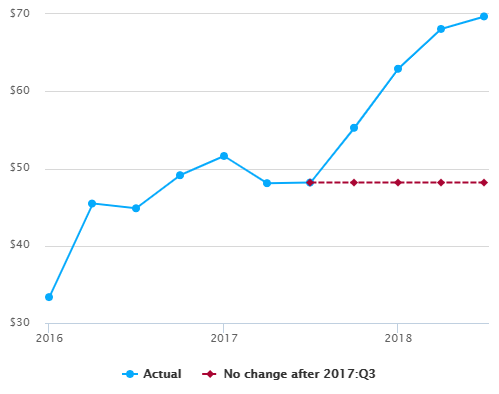

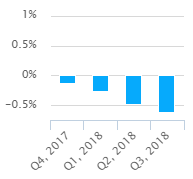

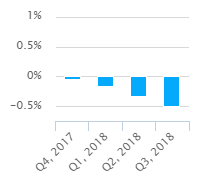

To determine the impact of the increase in oil prices over the last four quarters, I use the estimated coefficients to simulate a counterfactual in which WTI remains fixed at its third-quarter average of $48 per barrel, shown by the dashed line in Figure 5.

Source: FRED.

Sources: PWBM, BEA.

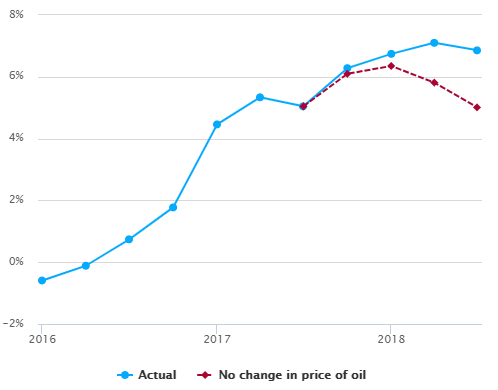

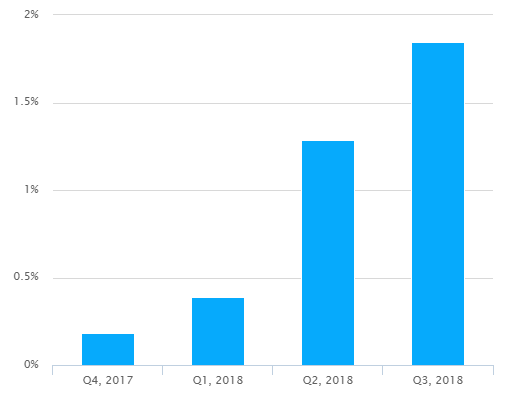

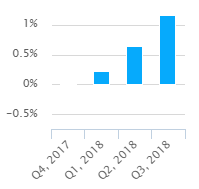

Figures 6 and 7 show the results. I estimate that the increase in oil prices added about 1¾ percentage points to growth in business investment over the last four quarters. Without it, investment would have grown 5 percent year-over-year in the third quarter, the same rate as in 2017. The response to the rise in oil prices explains the entire increase in the growth rate of investment in 2018.

Source: PWBM.

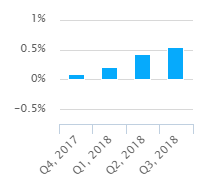

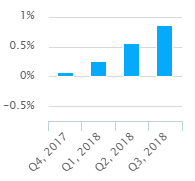

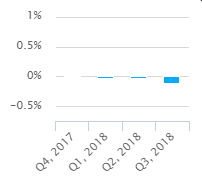

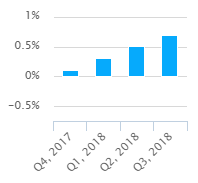

Figure 8 shows the estimated effect of the rise in oil prices on the different types of assets. As expected, oil-related equipment and structures account for most of the increase, with some positive spillovers to other assets. However, these gains are partially offset by declining investment in manufacturing, transportation, and commercial structures.

Commercial and health care

Computers and peripherals

Industrial equipment

Manufacturing structures

Mining, petroleum, gas structures

Office equipment and instruments

Oilfield and other equipment

Other structures

Power and communication

Transportation equipment

Source: PWBM.

-

https://www.eia.gov/dnav/pet/hist/LeafHandler.ashx?n=PET&s=WCRFPUS2&f=W ↩

-

For a more complete discussion of the effects of oil on the US economy, see Baumeister and Kilian (2016), https://www.brookings.edu/bpea-articles/lower-oil-prices-and-the-u-s-economy-is-this-time-different ↩

-

Most of this increase has since been reversed. On December 17, the price of WTI fell below $50. ↩

-

Including a more detailed breakdown of industrial production or proxies for non-industrial demand (such as personal consumption expenditures for services or the ISM non-manufacturing index) does not meaningfully affect the results. ↩

-

See section 5.3 of the NIPAs. ↩

-

Fitted values for total nonresidential investment include actual rather than predicted values for intellectual property products, which are not modeled. ↩

,Contribution

7/1/87,0.0087337099

10/1/87,0.0099390859

1/1/88,0.0071266529

4/1/88,0.010022894

7/1/88,0.0016081846

10/1/88,-0.0020301057

1/1/89,-0.0022529818

4/1/89,-0.0007239223

7/1/89,0.002170897

10/1/89,0.001836596

1/1/90,0.0064796528

4/1/90,0.0032873965

7/1/90,0.0008774159

10/1/90,0.0017573922

1/1/91,0.0014937613

4/1/91,0.0006026473

7/1/91,-0.0047129533

10/1/91,-0.0038417778

1/1/92,-0.0096426431

4/1/92,-0.0096193224

7/1/92,-0.0008455228

10/1/92,0.0007708966

1/1/93,0.0057899611

4/1/93,0.0061463158

7/1/93,0.0056298623

10/1/93,0.0061264789

1/1/94,0.0009552199

4/1/94,0.0009760864

7/1/94,0.0008687765

10/1/94,-0.0001977898

1/1/95,0.0005559539

4/1/95,-0.0009414135

7/1/95,-0.0021875012

10/1/95,-0.0039782238

1/1/96,-0.0013157685

4/1/96,0.0013785149

7/1/96,0.0016128917

10/1/96,0.0021067509

1/1/97,0.0046366679

4/1/97,0.0043137261

7/1/97,0.0040114221

10/1/97,0.0041616569

1/1/98,-0.000828545

4/1/98,-0.0013524316

7/1/98,-0.0006032765

10/1/98,-0.0023283322

1/1/99,-0.0007170017

4/1/99,0.0008349341

7/1/99,-0.0003467023

10/1/99,0.0022633285

1/1/00,0.0028687276

4/1/00,0.0025185035

7/1/00,0.0039239867

10/1/00,0.0035338425

1/1/01,0.0050701721

4/1/01,0.0041242571

7/1/01,0.0038927838

10/1/01,-0.0007178865

1/1/02,-0.0080402861

4/1/02,-0.0106055752

7/1/02,-0.0105361345

10/1/02,-0.0060983292

1/1/03,0.0014405582

4/1/03,0.0051861975

7/1/03,0.0042821676

10/1/03,0.0051420963

1/1/04,0.002853671

4/1/04,0.0007832433

7/1/04,0.0012697962

10/1/04,0.0012534551

1/1/05,0.0041945531

4/1/05,0.005130123

7/1/05,0.0047103708

10/1/05,0.0040658047

1/1/06,0.0052310464

4/1/06,0.0048506949

7/1/06,0.0047187491

10/1/06,0.0054009747

1/1/07,0.0021307307

4/1/07,0.0022212159

7/1/07,0.0030363807

10/1/07,0.0028411347

1/1/08,0.002370156

4/1/08,0.0044683838

7/1/08,0.0053800129

10/1/08,0.0055063783

1/1/09,-0.0032558073

4/1/09,-0.0189399575

7/1/09,-0.0275821558

10/1/09,-0.0289300219

1/1/10,-0.0120913671

4/1/10,0.0089228575

7/1/10,0.0184373801

10/1/10,0.0185577436

1/1/11,0.0152933702

4/1/11,0.0132493731

7/1/11,0.0154575309

10/1/11,0.021059369

1/1/12,0.0230035691

4/1/12,0.0213440476

7/1/12,0.012675247

10/1/12,0.0032746029

1/1/13,0.0002871466

4/1/13,-0.0003455806

7/1/13,0.0023177413

10/1/13,0.0014324517

1/1/14,0.0040561401

4/1/14,0.0089078975

7/1/14,0.0080934286

10/1/14,0.0099959512

1/1/15,-0.0039465298

4/1/15,-0.0248429179

7/1/15,-0.0339689924

10/1/15,-0.042497855

1/1/16,-0.039056997

4/1/16,-0.0297441099

7/1/16,-0.0216828288

10/1/16,-0.0133085924

1/1/17,0.0040117639

4/1/17,0.0169496186

7/1/17,0.0192184423

10/1/17,0.0191782723

,Oil-related investment,West Texas Intermediate (WTI)

10/1/09,-0.355463859,0.295114444

1/1/10,-0.163487213,0.82678832

4/1/10,0.160327163,0.305481659

7/1/10,0.376779922,0.116286696

10/1/10,0.370643946,0.120560129

1/1/11,0.260070672,0.193625824

4/1/11,0.20349062,0.311063334

7/1/11,0.227123421,0.176578738

10/1/11,0.310109486,0.103977461

1/1/12,0.324771465,0.09480633

4/1/12,0.285326663,-0.085599553

7/1/12,0.160380688,0.029890256

10/1/12,0.037915919,-0.063873495

1/1/13,0.003156291,-0.084077889

4/1/13,-0.003705118,0.008148638

7/1/13,0.025582271,0.148235197

10/1/13,0.016602893,0.107789406

1/1/14,0.04656718,0.046145493

4/1/14,0.098877972,0.098862597

7/1/14,0.090703937,-0.075222016

10/1/14,0.119714193,-0.249090114

1/1/15,-0.044350824,-0.508652899

4/1/15,-0.253581622,-0.440189837

7/1/15,-0.342951481,-0.525020515

10/1/15,-0.41955786,-0.427184176

1/1/16,-0.437067625,-0.312124696

4/1/16,-0.415860869,-0.21422631

7/1/16,-0.345348539,-0.035155003

10/1/16,-0.241606766,0.171663881

1/1/17,0.083419234,0.547781087

4/1/17,0.414638757,0.058142283

7/1/17,0.486912861,0.07424214

10/1/17,0.501871795,0.124763369

1/1/18,0.258771367,0.218600645

4/1/18,0.234719967,0.414970445

,Correlation Coefficient

1/1/95,-0.240413309

4/1/95,-0.187993734

7/1/95,-0.173790855

10/1/95,-0.158260806

1/1/96,-0.166973348

4/1/96,-0.15448812

7/1/96,-0.135382174

10/1/96,-0.083744138

1/1/97,-0.012645612

4/1/97,0.003810654

7/1/97,-0.03062956

10/1/97,-0.044571737

1/1/98,-0.063676017

4/1/98,-0.098355534

7/1/98,-0.148488208

10/1/98,-0.111019372

1/1/99,0.084111372

4/1/99,0.105767434

7/1/99,0.297305347

10/1/99,0.238154758

1/1/00,0.126854356

4/1/00,0.137455852

7/1/00,0.113701073

10/1/00,0.086409038

1/1/01,0.013361541

4/1/01,0.042910387

7/1/01,0.066221752

10/1/01,0.126834198

1/1/02,0.228062881

4/1/02,0.279022869

7/1/02,0.290811613

10/1/02,0.283542209

1/1/03,0.247222694

4/1/03,0.208735027

7/1/03,0.211445387

10/1/03,0.21497691

1/1/04,0.216175702

4/1/04,0.218535253

7/1/04,0.220947031

10/1/04,0.217753428

1/1/05,0.221032234

4/1/05,0.231359571

7/1/05,0.26472226

10/1/05,0.291252083

1/1/06,0.332846724

4/1/06,0.407632687

7/1/06,0.459884213

10/1/06,0.534278065

1/1/07,0.617952025

4/1/07,0.654937799

7/1/07,0.647539677

10/1/07,0.623445734

1/1/08,0.607069003

4/1/08,0.573071601

7/1/08,0.451457625

10/1/08,0.332234589

1/1/09,0.429443293

4/1/09,0.531433025

7/1/09,0.59070341

10/1/09,0.609633623

1/1/10,0.578181497

4/1/10,0.546526549

7/1/10,0.536028557

10/1/10,0.51726479

1/1/11,0.522649745

4/1/11,0.535757654

7/1/11,0.539046446

10/1/11,0.538930924

1/1/12,0.517540024

4/1/12,0.499457367

7/1/12,0.481068513

10/1/12,0.47342279

1/1/13,0.457781715

4/1/13,0.450885498

7/1/13,0.442692498

10/1/13,0.439795588

1/1/14,0.435738499

4/1/14,0.425080756

7/1/14,0.41540309

10/1/14,0.407961322

1/1/15,0.401447726

4/1/15,0.397300778

7/1/15,0.406202165

10/1/15,0.413506118

1/1/16,0.413294875

4/1/16,0.429013832

7/1/16,0.507122572

10/1/16,0.632501412

1/1/17,0.624288935

4/1/17,0.55588011

7/1/17,0.496442375

10/1/17,0.438036753

1/1/18,0.548187233

4/1/18,0.687295482

7/1/18,0.673253418

,Actual,Model

1/1/12,0.128585916,0.135805655

4/1/12,0.12514852,0.112949696

7/1/12,0.071333992,0.080548513

10/1/12,0.056517719,0.068785805

1/1/13,0.043640763,0.027255216

4/1/13,0.023353322,0.031845234

7/1/13,0.04429937,0.042460711

10/1/13,0.054214216,0.046990947

1/1/14,0.054783918,0.056429187

4/1/14,0.076004025,0.089387162

7/1/14,0.08013261,0.089460226

10/1/14,0.063435968,0.070163207

1/1/15,0.04559955,0.062947404

4/1/15,0.026989856,0.024819589

7/1/15,0.007968139,0.00701685

10/1/15,-0.007557815,-0.001803291

1/1/16,-0.005919774,-0.022373902

4/1/16,-0.001152994,-0.006566744

7/1/16,0.007394402,0.009008385

10/1/16,0.017727755,0.031585829

1/1/17,0.04460462,0.049591663

4/1/17,0.05336874,0.060025951

7/1/17,0.050445072,0.053065862

10/1/17,0.062797686,0.059236959

,Actual,No change after 2017:Q3

1/1/16,33.3518,

4/1/16,45.46063,

7/1/16,44.85187,

10/1/16,49.13556,

1/1/17,51.62129,

4/1/17,48.10381,

7/1/17,48.18177,48.18177

10/1/17,55.26587,48.18177

1/1/18,62.90574,48.18177

4/1/18,68.06547,48.18177

7/1/18,69.6873,48.18177

,Actual,No change in price of oil

1/1/16,-0.005919774,

4/1/16,-0.001152994,

7/1/16,0.007394402,

10/1/16,0.017727755,

1/1/17,0.04460462,

4/1/17,0.05336874,

7/1/17,0.050445072,0.05044507

10/1/17,0.062797686,0.06096452

1/1/18,0.067425739,0.06351208

4/1/18,0.070991908,0.05812857

7/1/18,0.068560724,0.05009394

,Oil price effect

2017 Q4,0.001833169

2018 Q1,0.00391366

2018 Q2,0.012863337

2018 Q3,0.01846678

,Data

2017 Q4,-0.0001783139

2018 Q1,-0.0013359417

2018 Q2,-0.0016543731

2018 Q3,-0.0027251315

2017 Q4,0.0003184641

2018 Q1,0.0001880198

2018 Q2,0.0010036488

2018 Q3,0.0009246681

2017 Q4,0.0004444341

2018 Q1,-0.0002998371

2018 Q2,0.0006248569

2018 Q3,-0.0001950367

2017 Q4,-0.001234481

2018 Q1,-0.002683457

2018 Q2,-0.004883533

2018 Q3,-0.006077847

2017 Q4,0.0001711245

2018 Q1,0.0022652564

2018 Q2,0.0065201595

2018 Q3,0.0116286412

2017 Q4,0.000873067

2018 Q1,0.002003289

2018 Q2,0.004185956

2018 Q3,0.00551334

2017 Q4,0.0007123841

2018 Q1,0.0026257731

2018 Q2,0.0055264916

2018 Q3,0.0085566202

2017 Q4,0.0001791192

2018 Q1,-0.0001959095

2018 Q2,-0.0003131666

2018 Q3,-0.0010530906

2017 Q4,0.001013598

2018 Q1,0.003026244

2018 Q2,0.005117113

2018 Q3,0.006871552

2017 Q4,-0.0004662271

2018 Q1,-0.0016797776

2018 Q2,-0.0032638169

2018 Q3,-0.004976932